Julie

and Robin Sharp's "brief and childless marriage" began to unravel when

she discovered he was "pursuing another relationship"

Julie Sharp is fighting the divorce settlement (Photo: NEV AYLING)

A city trader who made millions in "eye-watering" bonuses is fighting for a "fair" divorce settlement - after her ex walked away with nearly half the £7million fortune she earned.

Millionaire Julie Sharp was married to ex-husband Robin for four years after they set up home together in 2007.

When

they met, both were already earning around £100,000 - with Mr Sharp

working as an IT consultant and Mrs Sharp a successful energy trader.

But as the relationship took off she began to rake in massive bonuses due to the "soaring" energy market, Gloucester Live reported .

She amassed bonuses totalling £10.5million in just five years, London's Civil Appeal Court heard.

On

the strength of her "windfall", they bought two lavish country houses

in Gloucestershire - the second with a £2million price tag which cost

£500,000 to refurbish.

Mrs Sharp, now 44, took pleasure in giving her partner expensive presents - including a top-of-the-range Aston Martin.

But despite her sudden wealth she was adamant that her husband "didn't see her as a sort of cash machine". Divorcee dragged screaming from court after hearing she might lose home to ex-husband 10 years AFTER they split

In

September 2013, Mrs Sharp learnt that her husband "had been pursuing a

new relationship for some time", her QC Frank Feehan, explained.

Their "brief and childless marriage" began to unravel - with Mrs Sharp petitioning for divorce in December 2013.

Their

rows over money were hammered out before High Court judge, Sir Peter

Singer, who in November 2015 allocated Mr Sharp £2,737,000 in a "clean

break" award.

The couple's total assets amounted to around £6.9million - with virtually all the wealth stemming from the wife.

Mrs

Sharp, a mathematics graduate from a "modest financial background" who

worked diligently to carve out her high-flying career, is now appealing

that ruling.

Mr Feehan criticised the judge's approach as

"intrinsically unfair" in light of the brevity of the marriage, lack of

children, and her massive financial contribution.

Despite her

stellar earnings, the judge approached the case on the basis of a 50/50

split, although he reduced Mr Sharp's payout to reflect "unmingled"

assets that his wife built up before the marriage.

"The notion

that equal sharing applied in this case made for an unprincipled

decision," Mr Feehan told three Appeal Court judges.

Mrs Sharp had proposed that her ex should walk away with £1,197,000, which would more than cover his needs, he added.

Throughout

their time together the couple maintained largely separate finances, he

added, "earning and spending their own money".

They took turns

to pick up the bill when dining out and, during the marriage, Mr Sharp

himself accepted the "bonuses were not his".

He "went out of his

way to explain that he did not see her as a sort of cash machine on

whose financial resources he would have a call", said Mr Feehan.

And although Mrs Sharp had shelled out on "expensive gifts" for her spouse this did not reflect "shared finances", said the QC.

Robin Sharp was awarded nearly half of his wife's fortune (Photo: Richard Gittins / Champion News) One of her gifts was an Aston Martin, but Mr Feehan termed

this a "very lavish 'boy's toy' which she was happy to give out of

love".

It was her wealth which enabled the couple to buy their

two luxury homes, the court heard - the first of which was acquired by

her before they wed.

However, Mr Sharp, aged 43, insists he made a

major contribution by project managing and carrying out renovation

works on their two properties - particularly after he took redundancy in

2012.

That was after Mrs Sharp bought their second home - in

Shurdington, near Cheltenham, a sprawling six-bedroom manor house with

two acres attached.

Mr Sharp's QC, Jonathan Southgate, said he

deserved half of the marital pot and there was ample evidence of the

couple's intentions to pool their resources.

Even though Mrs

Sharp had not paid her bonuses into a joint account this was common in

many "traditional" marriages where the breadwinner retains earnings and

"pays housekeeping to the other spouse", he argued.

Mr Sharp was

clear in his evidence that "they agreed he should take redundancy and

stay at home - redeveloping their home and supporting their joint life

together".

The couple originally met while Mrs Sharp was working as a coal industry specialist in Swindon, the Appeal Court heard.

She was earning £135,000 yearly, before bonuses, while her spouse, who at one time worked for Cisco, brought in £90,000.

There was no real "intermingling" of their cash during the

marriage, claimed Mr Feehan, although Mrs Sharp had paid large cash

instalments to her ex during 2013 towards home improvements.

"The documentary evidence is plain," argued the QC. "There was never a joint approach to funds in this marriage.

"The oral evidence is also plain: the husband accepted clearly that such was the way they lived their life together."

Mr Southgate, however, backed the High Court judge's handling of the case.

"The

judge found that the evidence did not support her case that there was a

deliberate and agreed intention to maintain separate finances," he told

the court.

Overall, the judge's ruling was in line with "the usual sharing approach to divorce", the QC argued.

And there were no compelling reasons to "depart from that approach".

Lords Justice McFarlane, McCombe and David Richards have now reserved their decision on Mrs Sharp's appeal.

The Government this week paved the way for firms to slash the pension payouts of 11 million workers

BP chief Bob Dudley gained a £4.4m perk (Photo: PA

Fatcat bosses are raking in massive pensions perks while millions of workers are facing hardship in old age, a Daily Mirror investigation has revealed.

The Government this week paved the way for firms to slash the pension payouts of 11 million workers.

Yet companies are pouring a packet into directors’ retirement funds.

Research by the Mirror and shareholder group Manifest found that the average FTSE 100 chief executive gets the equivalent of 30% of their salary in pension payments annually.

But firms put an average 6% of a shopfloor worker’s salary into their pension. That produces a paltry £1,300 a year, on average.

Antonio Horta Osorio has a 50% pension perk (Photo: Getty)

Primark boss George Weston got a 68% boost By contrast, George Weston, boss of Primark owner

Associated British Foods, may well pocket £550,000 a year when he

retires. He had £711,000 put into his pension pot in 2015.

Associated British Foods called his pension “a mathematical outcome of longevity of service, age and salary”.

BP’s

Bob Dudley had £4.4million pumped into his pension that year – more

than three times his salary. BP said the payment was distorted by the

fact that it was a US scheme.

Alison Cooper received £590,000 (Photo: PA)

Erik Engstrom is given 67% for his pension Business information firm RELX put £766,000 into chief

executive Erik Engstrom’s pension in 2015, while Alison Cooper, who runs

tobacco giant Imperial Brands, got a £590,000 boost. Taxpayer-saved

bank Lloyds put £568,000 into Antonio Horta-Osorio’s retirement pot last

year.

Tom McPhail, head of retirement policy at broker

Hargreaves Lansdown, said: “The system is grossly unfair. There is one

rule for senior executives and one for everyone else.”

Earlier

this week, a Government Green Paper proposed that troubled firms with

defined benefit schemes could “cut or renegotiate” their pensioners’

benefits, potentially affecting 11 million people.

Retirement

may seem like a long time from now, but it’s closer than you think.

Don’t keep putting off your plans to get your finances in order. A survey

conducted by the Employment Benefit Research Institute found that

American workers are falling behind when it comes to preparing for

retirement. You can start the planning process by taking an inventory of

your financial situation. Here are some important questions you must

answer before you retire.

1. Do you really have enough money to retire?

Retirement savings | iStock.com

Guessing won’t cut it when it comes to figuring out how much money

you’ll need to live comfortably in retirement. It’s not a good idea to

leave this part of retirement planning to chance, because it can be

difficult to catch up once you realize you’re off track. Among the

Americans surveyed in the Employment Benefit Research Institute study

who said they are not saving enough, 20% said they plan to save more

later, while 15% said they will have to work during retirement, and 14%

said they have no choice but to delay retirement. Not knowing how much

you need to retire means you’re not going to be saving enough in the

meantime. If you don’t know the answer to this question, there are

plenty of retirement tools available to help you figure this out. One tool recommended by the experts is the T. Rowe Price retirement income calculator.

If you come to the conclusion that you are indeed behind on

retirement savings, you can still maximize contributions each year. For

2016, you’re allowed to contribute a maximum of $18,000 to a 401(k). If

you’re age 50 or older you can make an additional catch-up contribution of $6,000.

2. How much debt do you have?

Debt | iStock.com

Take a moment to tally up all of your outstanding debt. Expenses such as high-interest credit cards

and a mortgage will deplete your retirement income. Once you know how

much you owe, make an effort to pay down as much of your debt as

possible before you finally hang up your work hat. It will be tough to

pay off debt once you’re retired and living on a fixed income, so take

care of repayment sooner rather than later.

You may be feeling good and healthy as ever right now, but your

chances of needing long-term care increase with age. Those turning 65

years old today have a 70% chance of needing some type of long-term

care, according to LongTermCare.gov. In addition, roughly 20% of today’s

65-year-olds will need long-term care for more than five years. In

light of these statistics, it would be in your best interest to have long-term care insurance.

4. When should you apply for social security?

Social security card | iStock.com

It depends. Experts are divided about whether you should delay Social

Security until you reach age 70. Those who say it’s a good move reason

that waiting will allow you to collect a higher monthly benefit. Whether

you choose to follow this advice depends on your individual situation.

Some experts say if money is tight once you finally retire, you might

want to apply for benefits sooner (age 62 is the earliest you can

collect Social Security benefits) rather than later. Other experts say

if you can afford to wait, and you’re in relatively good health, you may

want to wait it out until age 70.

Waiting until your full retirement age (age 67 if you were born in

1960 or later) to take Social Security benefits will yield a benefit

amount that’s roughly 30% higher than if you take benefits at 62.

Waiting until 70 results in a benefit that’s roughly another 32% higher.

On the other hand, if you’re not in such great health and you need the

money, by all means apply for your benefits when you’re eligible.

5. Where will you live?

House | iStock.com

You’ll need to move to a place where you can stretch your retirement

dollars. Retirement life will likely mean lower income and possibly

higher health care costs. Do your research or you’ll end up blowing

through your nest egg too quickly. Besides cost of living, you’ll also

need to consider weather and convenience. As you age, driving may not be

a possibility, so make sure to find a residence that will offer

adequate mobility. While doing your research, you’ll want to make sure

to stay away from these 10 worst retirement cities. Consider these 10 best places to retire instead.

6. What will your retirement expenses be?

Money and piggy bank | iStock.com

Account for expenses such as the retirement lifestyle you would like

to have as well as the cost of medical care. Remember that if you’re in

poor health now, you will most likely spend a pretty penny during your

golden years when it comes to health care costs. If you want to get a

better picture of your future expenses, start by filling out a

retirement expense worksheet like the one featured here on the Vanguard website.

7. Have you thought about your social life?

friends enjoying a meal | iStock.com/monkeybusinessimages

This may seem trivial, but once you stop working you’ll have contact

with fewer people. If most of your friends and former co-workers are

still working, they may have less time for you. They also may be more

focused on work, so there may be fewer experiences to share. Make sure

you’ve prepared for your social life after retirement. You can do this

by planning to connect with a local senior center or volunteering within

your community. Just make sure you plan to get out and socialize. A study

by the Institute of Economic Affairs found that retirement can increase

your clinical depression risk by 40%. This is because many workers

closely link their identity and sense of purpose to their jobs.

Financial problems

have a way of sneaking up on you. At first you may start borrowing

money to make a purchase or using your credit cards a little too often.

Before you know it, you’re facing a mountain of debt. You may be content

with denying you have a problem with managing money. However, burying

your head in the sand will catch up to you if you don’t take the proper

steps get things under control. Here are a few signs you’re headed for

financial disaster.

1. You often borrow money from friends and relatives

Money | Thinkstock

Many of us run into a financial snag from time to time, but if you find yourself constantly asking your friends and family for a loan,

and you have trouble paying them back — or at all — this is a warning

sign. In addition, borrowing money from loved ones and repaying late or

not returning the money can lead to even more strain in your personal

life.

2. Bill collectors are calling you — and it’s not to say hi

Phone call | Justin Sullivan/Getty Images

Ignoring your bills won’t make them go away. You may feel a temporary

sense of comfort and relief when you toss your bills into a pile on

your desk, but that won’t resolve the issue. Your money problems will

just continue to worsen. Soon enough, your creditors may come looking for you.

3. You rely heavily on credit

Using credit card | iStock.com

If you often reach for your credit card,

even for small purchases, this is an indication that you are spending

more than you earn. Relying too heavily on credit and maintaining a

balance from month to month can cause your debt to balloon, leading to

even more financial strain. When you get to a point where you can’t

afford basics like groceries or gas, it’s time to reevaluate your

budget.

4. You’re living paycheck to paycheck

Burning money | iStock.com

If you find that you frequently overdraft and you’re just barely

making it from one paycheck to the next, you are living on the financial

edge. Burning through your cash faster than you earn it is asking for

trouble. All it takes is one major financial emergency to put you in a

crisis. The key is not to wait until a crisis hits before taking action.

Once you start to see that you’re experiencing financial difficulty,

begin looking for ways to either spend less or bring in more money.

5. You tell financial lies

Lying about money | iStock.com

Are you making purchases and lying to your partner about it? Are

you gambling your paycheck away or excessively shopping? If you have

lost control of your spending and you’re going to great lengths to

conceal your behavior, this could put you at risk for serious financial

trouble down the road. Furthermore, taking a reckless approach to money

could point to some areas that need to be addressed concerning your

mental health. Meeting with a therapist may help you figure out if you have a deeper problem that requires exploration.

Warren Buffett

is no stranger to multibillion-dollar investments. The Oracle of Omaha

has been beating the market for decades while accumulating positions in

some of the world’s most popular companies. Courtesy of a new filing, we now have a peek at how the legendary investor deployed capital in the final three months before 2017.

Many institutional investment managers recently filed their mandatory

13F with the Securities & Exchange Commission (SEC). The filing is a

quarterly report of equity holdings required by managers who oversee

more than $100 million in qualifying assets and must be filed within 45

days of the end of each quarter. The 13F provides a glance at what firms

did in the previous quarter, but investors should keep in mind that

hedging and trading strategies of each fund are still unknown.

Buffett’s Berkshire Hathaway made several big changes in the three

months ended December 31, 2016. In fact, this was one of the most

exciting 13F releases from Buffett and company in recent history.

Buffett also recently disclosed that Berkshire Hathaway purchased a net $12 billion in stock since the presidential election.

The conglomerate sold off its stakes in Deere and Kinder Morgan, two

positions that had already been reduced in a prior 13F release.

Berkshire Hathaway decreased its stakes in Verizon and Wal-Mart, but

opened new positions in Monsanto, Siri XM, and Southwest Airlines.

The largest investments in Berkshire Hathaway’s portfolio include

some of the most popular blue chips known to Wall Street. Let’s take a

look at Berkshire Hathaway’s top nine holdings according to dollar value

at the end of December, not including Buffett’s option to purchase 700

million shares of Bank of America at any time prior to September 2021

for $5 billion. No. 7 is new to our Cheat Sheet list of Buffett’s

biggest holdings, but it’s one of the most loved companies in the world.

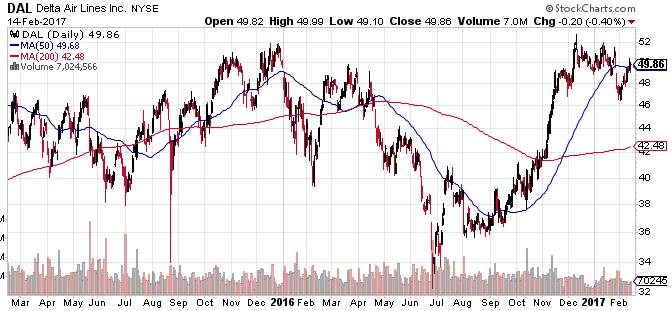

9. Delta Air Lines

DAL stock price | StockCharts.com

A few years ago, Buffett called airlines a “death trap for

investors.” Times have changed. Buffett hasn’t said exactly why he likes

airline companies so much now, but the evidence is clear, he’s bullish

on the industry. At the end of the fourth quarter, Berkshire Hathaway

held about 60 million shares of Delta, worth $3 billion, and

significantly greater than the 6.3 million shares held in the prior

quarter. Investors should also keep in mind that Berkshire Hathaway

opened a new position in Southwest Airlines, and increased its stakes in

American Airlines and United Continental during the fourth quarter.

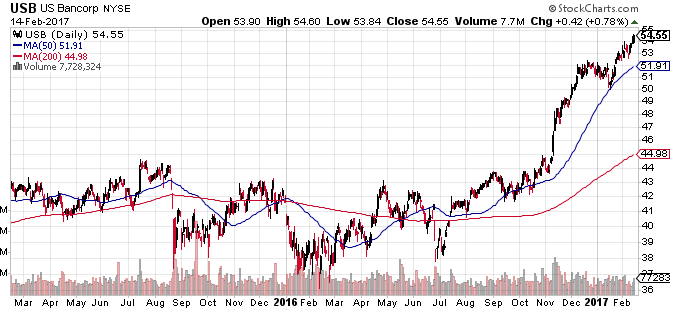

8. U.S. Bancorp

USB stock price | StockCharts.com

The financial industry is no stranger to Buffett. Berkshire Hathaway

held 85.1 million shares of U.S. Bancorp at the end of the fourth

quarter, worth $4.4 billion. The position is unchanged from the prior

quarter, but a recent rally in share price continues to keep U.S.

Bancorp as one of Berkshire Hathaway’s largest holdings.

U.S. Bancorp is based in Minneapolis and has nearly half a trillion

dollars in assets. It’s the parent company of U.S. Bank National

Association, the fifth largest commercial bank in the United States. The

Company operates 3,106 banking offices in 25 states and 4,842 ATMs. In

October, MONEY named U.S. Bank the Best Big Bank in a tie with TD Bank.

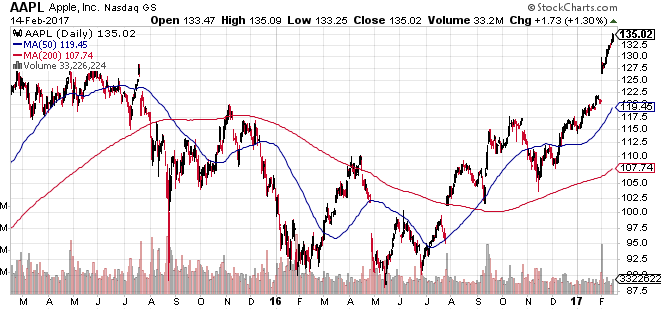

7. Apple

AAPL stock price | StockCharts.com

The beloved Apple is on our Buffett Cheat Sheet list for the first

time. Berkshire Hathaway more than tripled its prior stake and now owns

57.4 million shares of the tech giant, worth $6.6 billion, as of the end

of 2016.

Despite concerns about growth, Apple doesn’t appear to be slowing

down. The company sold 78 million iPhones in the holiday quarter,

setting a new record. Apple also set new revenue records for the iPhone,

Services, Mac, and Apple Watch. Furthermore, Apple’s cash hoard of $246

billion will likely continue to reward investors with dividends and

share buybacks for years to come. Apple returned $15 billion to

investors in the fourth quarter alone.

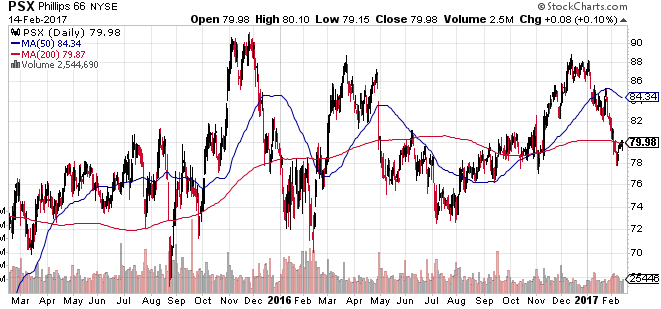

6. Phillips 66

PSX stock price | StockCharts.com

The multinational American energy company was originally thought to

be sold off by Buffett in the second quarter of 2015. As it turns out,

Buffett had the stake classified as confidential so it wouldn’t show on

the 13F and allow copycat investors to run the price up. At the end of

December, Berkshire Hathaway held 80.7 million shares (worth $7

billion), unchanged the previous quarter, according to the 13F. Phillips

66 is Berkshire Hathaway’s No. 6 largest holding, and appears to be a

favorite, especially when its share price dips toward $75.

Unlike oil giants Exxon Mobil and Chevron, Phillips 66 has escaped most of the carnage seen in the energy sector. Buffett told CNBC in 2015: “We’re buying it because we like the company and we like the management very much.”

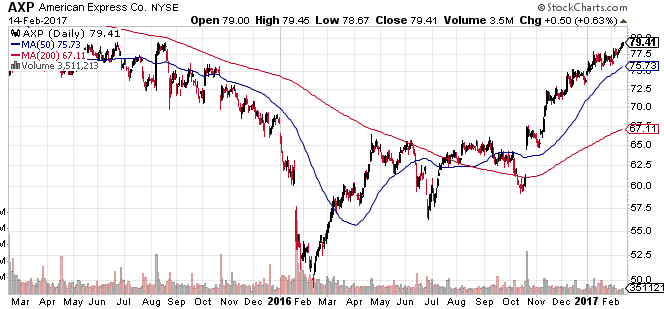

5. American Express

AXP stock price | StockCharts.com

Warren Buffett has liked American Express since at least the 1960s.

Today, the credit card giant is Berkshire Hathaway’s No. 5 largest

holding. At the end of the fourth quarter, Berkshire Hathaway held 151.6

million shares (worth $11.2 billion), unchanged from the prior quarter.

American Express shares have struggled in recent years. Costco

severed ties from American Express after 16 years in business with each

other. American Express was able to make a deal with Sam’s Club, but it

did little to comfort Mr. Market at the time. However, shares found a

bottom in early 2016 after touching $50, and are in the green this year.

Berkshire Hathaway’s positions in Mastercard and Visa come nowhere

close to the size of its American Express position.

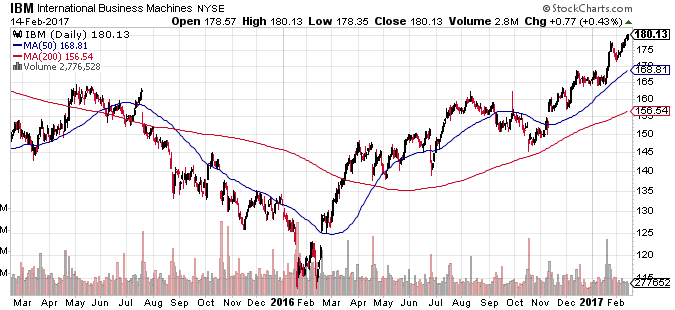

4. International Business Machines

IBM stock price | StockCharts.com

If you’re looking for a reason not to follow in Buffett’s footsteps,

IBM used to be it. The company was the worst performer in the Dow Jones

Industrial Average in 2014, and one of the worst performers in 2015. In

fact, IBM’s revenue has fallen for 19 consecutive quarters. Nonetheless,

Buffett isn’t giving up and you might not want to either. IBM’s stock

price has surged from $115 to $180 over the past year, providing yet

another example why thinking about the long-term may help you avoid

making bad investing decisions.

IBM is Berkshire Hathaway’s No. 4 largest holding. At the end of the

fourth quarter, the company held 81.2 million shares (worth $13.5

billion). IBM shares still offer a dividend north of 3%.

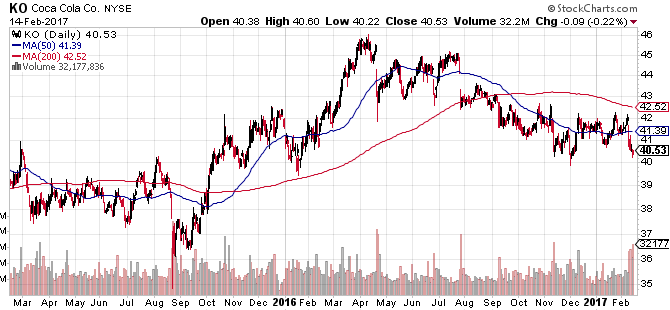

3. Coca-Cola

KO stock price | StockCharts.com

Coca-Cola is the most predictable position at Berkshire Hathaway.

Buffett is on record saying he will never sell his shares in the

world-renowned beverage company, and can often be seen holding a Cherry

Coke. At the end of the fourth quarter, Berkshire Hathaway held the

usual 400 million shares of Coca-Cola (worth $16.6 billion), making it

the company’s No. 3 largest holding.

While sugar water has seen its fair share of problems in recent

years, Coca-Cola shares have been experiencing support near $40 since

late 2015. Coca-Cola has investments in Monster Beverage, Keurig Green

Mountain, and Suja Juice. The company is also making operating changes

to drive stronger growth and save $3 billion annually by 2019.

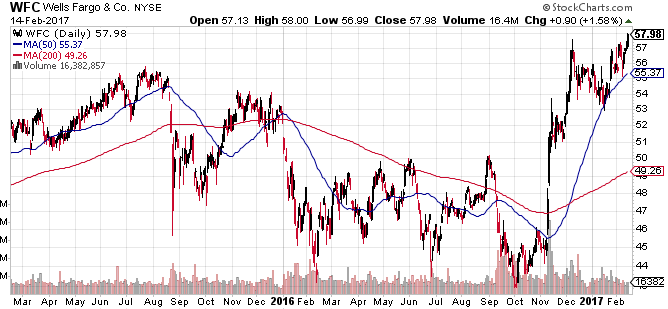

2. Wells Fargo

WFC stock price | StockCharts.com

America’s second most profitable bank is also Buffett’s No. 2 largest

holding. Berkshire Hathaway held 479.7 million shares (worth $26.4

billion) of Wells Fargo at the end of the fourth quarter. Somewhat

surprisingly, this was once again unchanged from the prior quarter.

Wells Fargo quickly become Buffett’s most controversial holding in

September. The mega bank finally admitted it created roughly 2 million

fake accounts, which inflated sales numbers and banking fees. Wells

Fargo had an incentive program in place that essentially forced

employees to commit fraud or risk being fired for underperforming

unrealistic sales goals. More than 5,000 workers related to the scandal

were fired. Wells Fargo CEO John Stumpf also resigned in the wake of the

financial abuse. Buffett appears to be standing by Wells Fargo for now.

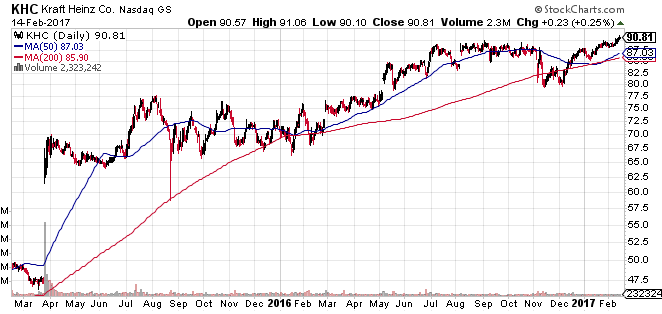

1. Kraft Heinz

KHC stock price | StockCharts.com

Berkshire Hathaway’s position in the merged Kraft Heinz has been

listed on the 13F for the past six quarters. Buffett teamed up with

investment firm 3G Capital to takeover Kraft Foods with Heinz. The deal

created one of the biggest food companies in history, with over 10

different brands valued at more than $500 million each. More recently,

the company has laid off thousands

of workers to cut costs and “consolidate manufacturing across the Kraft

Heinz North American network.” In August, Kraft Heinz raised its

quarterly dividend 4.3% to $0.60 per share.

Buffett and company held 325.6 million shares of Kraft Heinz at the

end of December, worth a whopping $28.4 billion. That makes it Buffett’s

largest portfolio holding. Disclosure: Author holds BRKB and AAPL

Too much debt can ruin your life. You may not be able to get a

mortgage for a house, you might face never-ending credit card payments,

and you might even face court action if you can’t pay your bills. Even a

small amount of debt can bring on obnoxious collector calls and make it

difficult to build your credit. If you have wanted to eliminate or cut

your debt, and you’ve tried, but you can never seem to really get your

debt in control, then something might be in your way. Some people find

that it is difficult to cut debt on a limited budget,

but it is possible to do so with careful planning and smart lifestyle

changes. In addition, if you’re currently overspending, using credit

cards too often, or not keeping a budget, all of these choices can make

it difficult to get out of debt.

1. You don’t keep a budget

Keeping a budget is essential in order to become financially stable,

and to eventually get out of debt. Even if you regularly pay your loan

payments, you won’t be able to pay much extra, or even pay every month,

if you don’t keep track of your spending and stay in budget. Without

regular budgeting updates, you won’t know how much you are spending, or

how much extra you have. This will make it difficult to prioritize

cutting down your debt, because if you are overspending each month, you

will risk going even further into debt.

A Gallup poll found that only one in three

Americans keeps a detailed household budget each month. If you are part

of this group, and you want to get out of debt, then maintaining your

budget is a great place to start.

2. You don’t set financial goals

Person Hand Inserting Coin In Pink Piggybank | iStock.com/AndreyPopov

Setting financial goals specifically about your debt will help you

have a date in mind to pay off your debt. If you owe a lot of money, it

can feel like you will never pay it off. However, setting a specific

goal will allow you to plan for how much you need to pay off each month

in order to meet your goal. In addition, knowing a due date will help

you visualize the debt disappearing, which can help motivate you to keep

up with your payments.

According to a poll by CreditCards.com, 18% of those polled who were already in debt expected to still have loans when they died. Thinking like this will certainly not help you pay off your debt, but setting financial goals can.

3. You rely too heavily on credit cards

Credit card user | iStock.com

Credit cards can be helpful and even necessary, but they can also be

dangerous. Because of the high interest rates, using credit cards too

much (especially if you can’t immediately pay the minimum balance) can

truly destroy your budget, and leave you in a long-term debt cycle. The average credit card debt

includes $1,128 per card that doesn’t carry a balance, $1,164 per

account for U.S. adults with a credit report and a Social Security

number, $3,766 per person for U.S. resident adults, and $5,540 per U.S.

adult with a credit card.

If the majority of your debt is from credit cards, or you rely too heavily on credit cards, you can reduce your debt

by negotiating lower rates, tracking your progress, paying with cash,

and implementing other ideas such as those mentioned in this article

(like using a budget and making goals).

4. Your priorities are all wrong

Luxury yacht | iStock.com

It’s nice to have a big house and a fancy car, but if you can’t

afford to do so then taking out loans that you can’t afford is a bad

idea. If you purchase more house than you can buy, or you buy a car that

leads to an expensive monthly payment, it can be difficult to stay on

budget and reduce debt. If you are worried about keeping up with your

friends by buying fancy suits or shoes, or eating out all the time, you

will also find it difficult to eliminate your debt.

The good thing is that you can always change your spending habits. If

you’re willing to downgrade your house or your car, and you can stop

impulse or peer spending, you can get your finances back on track and

cut your debt. Too much debt can be hard to live with, but there are

ways to pay your debt down and still have the things you need (and even

some that you want). Doing so requires keeping a budget, changing your

spending habits, and making and keeping financial goals.

Americans today are pretty awful at saving money. Since 25% of Americans

said they would give up showers in order to save money, systemic issues

like income inequality are likely more to blame than individual habits.

But don’t let that be your excuse. Even when you are near-broke, you

can still find ways to save here and there. You can cut out unnecessary expenses, eat your meals at home, and make a strict budget and stick to it.

Are you getting bored yet?

It seems that for some people, no matter how many articles they read,

no matter how many advisers they meet with, today’s wants simply

outweigh tomorrow’s needs. That’s not to say there aren’t people who

have money troubles for no fault of their own. But if your steady income

is accompanied by a history of poor money management, unpaid debts, and bad financial choices in general, chances are good that you’re just a terrible saver.

To help you understand why you can’t seem to put any of your paycheck

aside, we’ve outlined some of the reasons people are so inept at

saving. If you can understand where you’ve gone wrong, it will help you

finally turn things around. Here are the major missteps of the

savings-challenged.

1. You keep upgrading your lifestyle

Fancy ride to the poor house | Aston Martin

When you get a tax refund or a bonus at work, is your first thought

to go out and splurge on a luxury? Impulse buying is one of the most

dangerous habits consumers can develop, and it can be made even easier

by sudden windfalls. This is how people get into the dangerous cycle of

unnecessarily living paycheck to paycheck. What happens is you justify

each purchase by telling yourself you still have money “left over.” You

might think of increased wealth as a chance to seek status symbols or

lifestyle upgrades. Instead, use your newly acquired wealth to break

free from old habits. If you resist the temptation to spend your entire

paycheck, you’ll find that a little security will give you much more

freedom than a lifestyle upgrade.

2. You procrastinate

Sleeping instead of taking action | iStock

There’s a reason why “pay yourself first,” is a golden rule of personal finance. It’s

because if people don’t set aside money right away, most won’t do it at

all. The general idea is this: Take a certain percentage of your

paycheck and allocate it to savings, and the remainder is what you’ll be

left with to use for bills and other expenses. Bad savers are often

procrastinators, so they continuously tell themselves they’ll save

later. To take the pressure off, these kinds of consumers can benefit

from setting up automatic withdrawals each month. This gives you no

choice but to save, so you can stop making excuses to put it off again

and again.

3. You think saving is lame

Shopping won’t solve your money problems | iStock.com

Bad savers sometimes claim they like to “live in the now,” rather

than prepare for the future. Do you ever feel like you are stuck in the

present? It’s often a lot less glamorous and exciting than it sounds.

You can’t have much fun living in the present moment if your present

always feels like you are running out of money. Savers are actually

better equipped to take the occasional spontaneous trip or adventure

because they don’t have to wait for their next paycheck every time they

want to do something fun. Instead of focusing on what you want in the

here and now, and being disappointed when you can’t afford it, start

thinking about what you really want. If you can see past your immediate

desires, your bigger goals will start to motivate you. Then you’ll see

that saving isn’t a chore at all, it’s your ticket to financial freedom.

A divorce and marriage counseling session in Old School | Source: Dreamworks

Maintaining a long, healthy relationship is

one of the biggest challenges people face in life. There are so many

factors that can affect the status of a marriage or relationship and so

many things that are simply out of a couple’s control that divorce has

become rather common. Though divorce rates have been slowing down over the past several years, people are still doing what they can to avoid it — be it marrying the right person, waiting until the right age, or deferring until financial security is solidified.

All of those things may help you avoid a divorce, but we now have

even more insight into what can make an otherwise strong union fracture.

And it has more to do with the economy than with Tinder profiles,

Facebook flirting, or too much time at the bar or in front of the Xbox.

According to a study published in American Sociological Review,

the biggest factor leading to divorce is the husband’s job status.

Harvard researcher Alexandra Killewald crunched the numbers and found

that men who didn’t have jobs, or who had been out of work for a long

time had a statistically higher chance of getting divorced in any given

year, compared to those with stable careers.

Many couples fight about money, and that is often a leading factor in

divorce proceedings. But this study goes a little deeper and adds

another layer of complexity to those financial issues. Per Killewald’s

study, men without jobs increase their odds of divorce by roughly 30%.

Divorce and employment status

Unemployed businessman | Source: iStock

The research looks at data dating back 46 years to the 1970s and

found that for men who were not employed full-time, there was a 3.3%

chance they would get divorced in any given year. Compare that to men

who did have a full-time job during the same time period, and the

chances dropped to 2.5%. That’s what was found from looking at more than

6,300 couples.

“For marriages formed after 1975, husbands’ lack of full-time

employment is associated with higher risk of divorce, but neither wives’

full-time employment nor wives’ share of household labor is associated

with divorce risk,” the study says. “Expectations of wives’ homemaking

may have eroded, but the husband breadwinner norm persists.”

Those are a couple of other interesting details that the study

unearthed — that the full-time job status of the wife and the division

of household labor didn’t have a significant impact on divorce risk.

Instead, the real difference had to do with the husband’s job status.

“It is possible that husbands’ less than fulltime employment is

associated with marital disruption more strongly than wives’, not

because of gendered interpretations of lack of full-time employment, but

because husbands’ part-time employment or nonemployment is more likely

to be involuntary,” the study says. “Involuntary nonemployment may

negatively affect marriages more strongly than voluntary nonemployment.”

In other words, it’s not just being out of work; it’s being fired or laid off, and not being able to find a job.

Dodging divorce

Wedding rings | iStock

There are limitations to the study, as Killewald points out. It

didn’t include same-sex couples (marriage data hasn’t existed for very

long), and it didn’t include men who chose to become stay-at-home dads,

and let their wives be the household breadwinner. Read through the study

to get a full picture of Killewald’s other concerns. There is also evidence out there

that division of labor in the household and a wife’s employment status

can play a bigger part in divorce than this study claims.

But what you really need to know is that there was a clear correlation with employment status and divorce rates.

What does this mean for you and your relationship? It might not mean

anything — each and every marriage and relationship is different. But

we’ve known for a long time that many marriages fail due to financial

problems, and the employment status of the husband clearly plays into

that.

And perhaps most importantly, there are innumerable other factors

that can lead to divorce that aren’t necessarily taken into account by

this study. Cultural differences, religion, children — a marriage can be

wrecked by any number of things, not merely the fact that someone loses

their job. But a connection exists, according to Killewald’s work, and

if you want to stay out of divorce court, you should first try to stay

out of the unemployment office.

Planning for retirement is a smart thing to do. However, it’s not always the most enjoyable activity. Reaching your retirement savings goal requires some sacrifice now so that you can enjoy life later. Even though getting ready for your golden years

means you’ll have to give up some things today, you’ll thank yourself

in a few years. However, not everyone thinks this way. Less than half of

workers in the United States (48%) said they and/or their spouse have

never attempted to calculate how much money they’ll need so they can

live comfortably during retirement, according to an Employee Benefit Research Institute survey.

Instead of focusing on the results, some people make excuses for why

they can’t save for retirement. Here are five of the lamest retirement

excuses people tell themselves.

1. I’ll work until I die

iZombie | The CW

If you reason that you can just put off retirement savings

because you plan to work until you die at your desk, you might want to

rethink that plan. The odds of being physically unable to work at some

point in your life are higher that you might expect. Roughly 1 in 4 of today’s 20-year-olds will become disabled before they have a chance to retire, according to the U.S. Social Security Administration. Sadly, many millennials say they expect to work until they draw their last breath. A survey

of adults aged 20 to 34 conducted by Manpower Group found that about

20% of millennials believe they will have to work until their dying day.

2. I need to save for my kids’ college education

College fund | iStock.com

Your kids can get a scholarship for college. You, on the other hand,

can’t get a scholarship for retirement. In addition, your child can

choose a less expensive option for school or take on a side job.

Transfer some of the responsibility for college financing to your

children. It will teach them a bit of responsibility. The best gift you

can give your children is to not be a burden on them when you’re older.

In this situation it’s best to put yourself ahead of the kids. Don’t

feel guilty, they’ll appreciate it later. Financial adviser Pedro Silva says many people put other major expenses before retirement and never get around to saving for the future.

People often cite car payments, child care expenses,

credit card, or college debt as primary concerns and retirement saving

as something to be done later. There is no way to make up for lost years

of retirement savings, and those who can afford to save the additional

amount later often take on too much risk to make up for the time lost.

We often picture our lives in the future as being different; we will

exercise, we will eat better, spend more time with our families, clean

out the basement, etc. The truth is the changes you wish to make have to

start today. Make a to-do list and write “call HR to start 401(K). Once

that is done, move on to the next item, realizing you are in control

and making choices to shape your future in the direction you want to go.

3. I’ll save when I make more money

Paying bills | iStock.com

Time is quickly ticking away. If you wait until you make more money,

you might be waiting for a very long time. Raises and promotions aren’t

guaranteed (neither is your job), so you might as well go ahead and

start socking away some cash now. The longer you wait to save, the less

time your money has to grow, so it’s wise to start saving as soon as

possible. If you delay saving for retirement until you’re 35 years old,

you’ll need to save more than 16% of your income

each year just to produce the same potential retirement income at the

age of 65 as a worker who started saving 10% of their income starting at

30 years old, according to the Insured Retirement Institute. If you

decide to wait until 40 years old, you would have to save more than 26%

of your income.

4. I can’t afford to save for retirement

Money in a wallet | iStock.com

Saving for retirement means you’ll have to give up some comforts right now, but you really can’t afford not

to save for retirement. If your finances are tight, work on developing a

budget so that you can make room for retirement savings. Your future

survival could depend on it.

Howard Dvorkin, CPA and Chairman of Debt.com said the people who

claim to not be able to afford retirement are usually the ones who are

wearing most of their money in the form of expensive purchases:

The lamest excuses I always hear are the unsaid ones. I

meet someone who tells me they simply can’t afford to save for

retirement, as they look at their Omega wristwatch and climb into their

leased BMW so they can pack for their vacation to the Bahamas. Yes, many

Americans are struggling and simply have trouble making ends meet, and I

respect and work with them. But I meet many other Americans who earn

quite enough to meet all their obligations – but they spend frivolously

without ever admitting it to themselves.

5. I don’t know how much to save

Thinking young woman looking up at many question marks | iStock.com/SIphotography

There are plenty of retirement tools available that can help you figure out how much cash to put away.

This is one of the worst excuses for not building your nest egg. These

tools allow you to create a retirement budget, figure out life insurance

needs, estimate retirement income, and more. As a general rule of

thumb, you should aim to have at least one times your salary saved by

age 30, three times by age 40, seven times by age 55 and 10 times your

salary by the time you reach 67 years of age, according to Fidelity.

Governor Godwin Obaseki of Edo State yesterday signed the 2017 appropriation Bill into law. The

governor who also signed the Pension Bill into law, said he would

organise the implementation of the Contributory Pension Scheme. Governor

Obaseki who commended the legislators for the ‘speedy’ passage of the

budget, said, “Last year when I presented this bill to you for

consideration, we were very clear that there were certain key principles

and budget policies, which we showed would lead to significant changes

in our economy. This early passage will help the process.” On

the pension bill, he said the state government had already commenced

implementation of the Contributory Pension Scheme since January and that

with the signing of the Pension Bill, what was left was to start

settling arrears.